The Income Squeeze in Ontario: When Rising Costs Outpace Paycheques

The Income Squeeze in Ontario: What’s Happening and Why It Matters

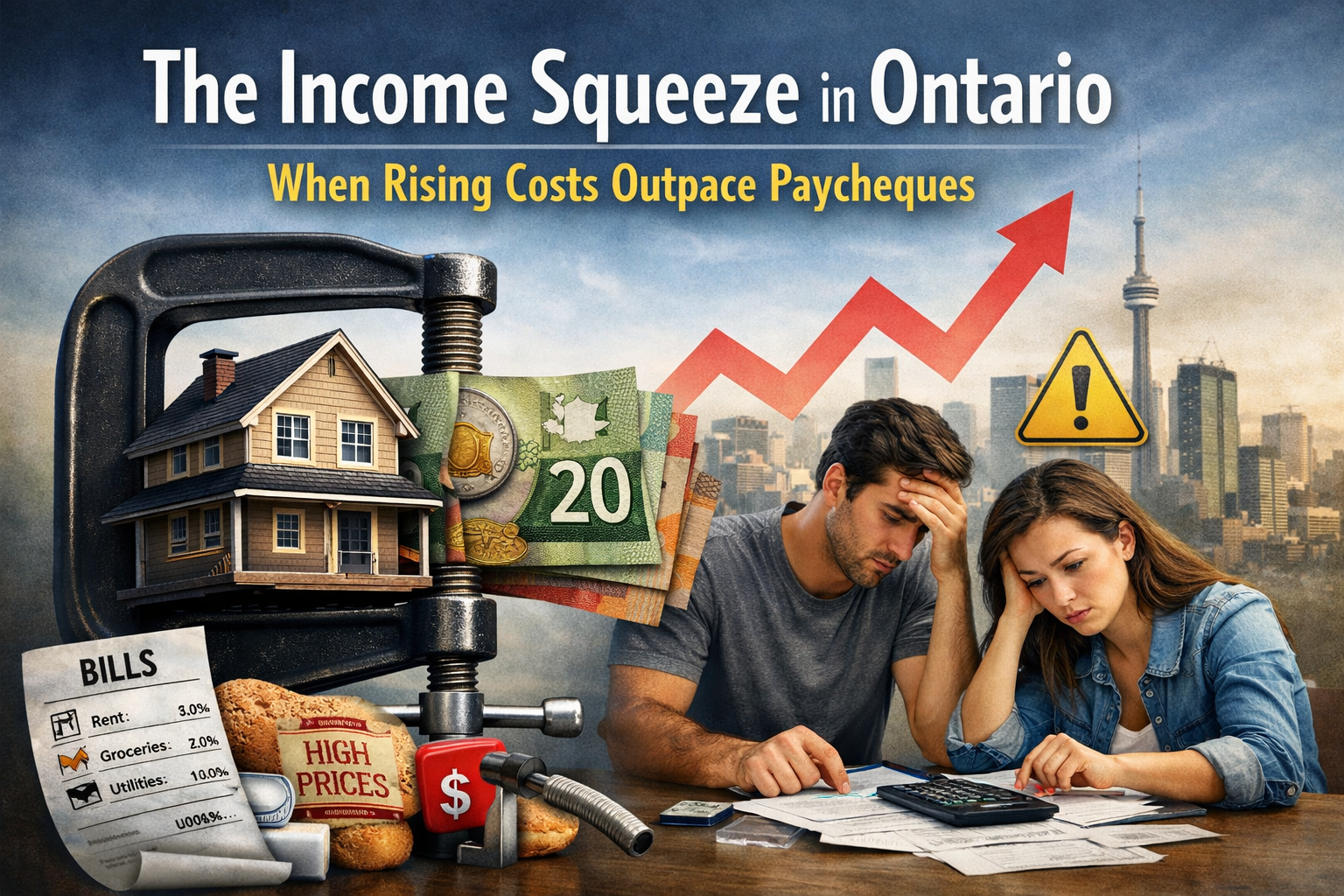

Ontario households are under sustained financial pressure. For many residents, the combination of rising costs and relatively stagnant income means less discretionary spending, deferred life goals, and tighter monthly budgets. This blog unpacks the income squeeze — what it is, what’s driving it, and how it’s affecting Ontarians in 2025–2026.

📌 1. Defining the “Income Squeeze”

Income squeeze refers to a condition where household income fails to keep pace with the cost of essentials — housing, food, utilities, and transportation. In practical terms:

• Wages and salaries have grown modestly.

• Meanwhile, prices on basic goods, rents, and especially shelter costs have climbed faster.

• As a result, households spend an increasing share of income just to maintain the same lifestyle.

This does not mean every family is worse off in absolute terms; rather, the relative burden of necessary expenses has increased.

📈 2. Core Drivers of the Income Squeeze

🏠 Housing Costs Outpacing Earnings

Housing is the largest component of most household budgets. In Ontario:

• Home prices in many cities have risen much faster than local median incomes over the past decade. In some regions, typical monthly mortgage payments can exceed 60–70% of after-tax family income.

• For younger workers or first-time buyers, homeownership is largely out of reach without significant outside financial support.

Renters also feel this pinch: even before a lease renewal, rents in many markets outpaced general inflation and consumed a disproportionate amount of household income.

💸 Rising Prices on Essentials

Inflation — especially for food, energy, and basic services — has pressured household wallets. Nearly half of Canadians report that rising prices have substantially affected their ability to meet day-to-day expenses.

📉 Wages Increasing Slowly

While wages have risen in recent years, growth rates often lag behind cost increases. Some analyses indicate that a living wage — the income necessary to cover basic expenses — remains well above the provincial minimum wage in all regions of Ontario.

👥 3. Who Is Most Squeezed?

The income squeeze does not affect all households equally:

• Lower-income households bear the brunt: they spend a larger share of income on essentials and have less buffer for unexpected costs.

• Young adults and households with children report more financial stress and higher concern over housing affordability.

• Renters vs. homeowners: renters are substantially more likely to spend over 30% of income on shelter than owners, a key indicator of housing unaffordability.

⚠️ 4. Implications for Ontarians

🧠 Financial Stress and Quality of Life

High cost pressures correlate with increased stress levels and reduced life satisfaction. Surveys show many households feel significant daily financial strain due to price increases.

🚗 Workforce and Mobility Issues

Household budget pressure affects labour markets. Workers who cannot afford to live near jobs may face long commutes, higher turnover, and reduced local economic participation.

📉 Long-Term Economic Impacts

When a majority of income is tied up in housing and necessities, consumer spending on other sectors weakens, dampening economic growth potential over time.

📌 5. What’s Not in Debate: It’s Real

The income squeeze in Ontario isn’t an abstract concept — it’s measurable:

• Price increases on essential goods and housing continue to outstrip nominal wage growth in most regions.

• Standard metrics of affordability show sharp divergence between housing costs and incomes.

• Quality of life surveys reveal tangible stress and financial strain tied to cost of living pressures.

📊 6. Bottom Line — Ontario’s Financial Crossroads

In 2025–2026, many Ontario households are struggling not because income fell, but because costs rose faster than what typical incomes can absorb. Housing remains the dominant factor, but the squeeze extends into food, utilities, and transportation — forcing households to make trade-offs and reevaluate long-term financial plans.

Contact

Rick Bettencourt, Mortgage Broker Level 2,

FSRA License #M11002425

licensed with Chartered Finance, Brokerage #12791

#302 – 7300 Warden Ave, Markham, Ontario.

Phone: (647) 952-1661

Helping Ontario homeowners access practical mortgage solutions with clarity and confidence.

© 2025 Pure Mortgage Advisory Services. All rights reserved.