Flexible approvals for self-employed, complex income, credit challenges, or time-sensitive situations.

An alternative mortgage is a financing solution for homeowners who don’t fit standard bank criteria. These products focus more on equity, overall financial strength, or unique income situations than strict credit and income tests.

• Often based on property equity rather than paycheque validation

• May accept non-traditional income sources

• Can be faster to fund when time is critical

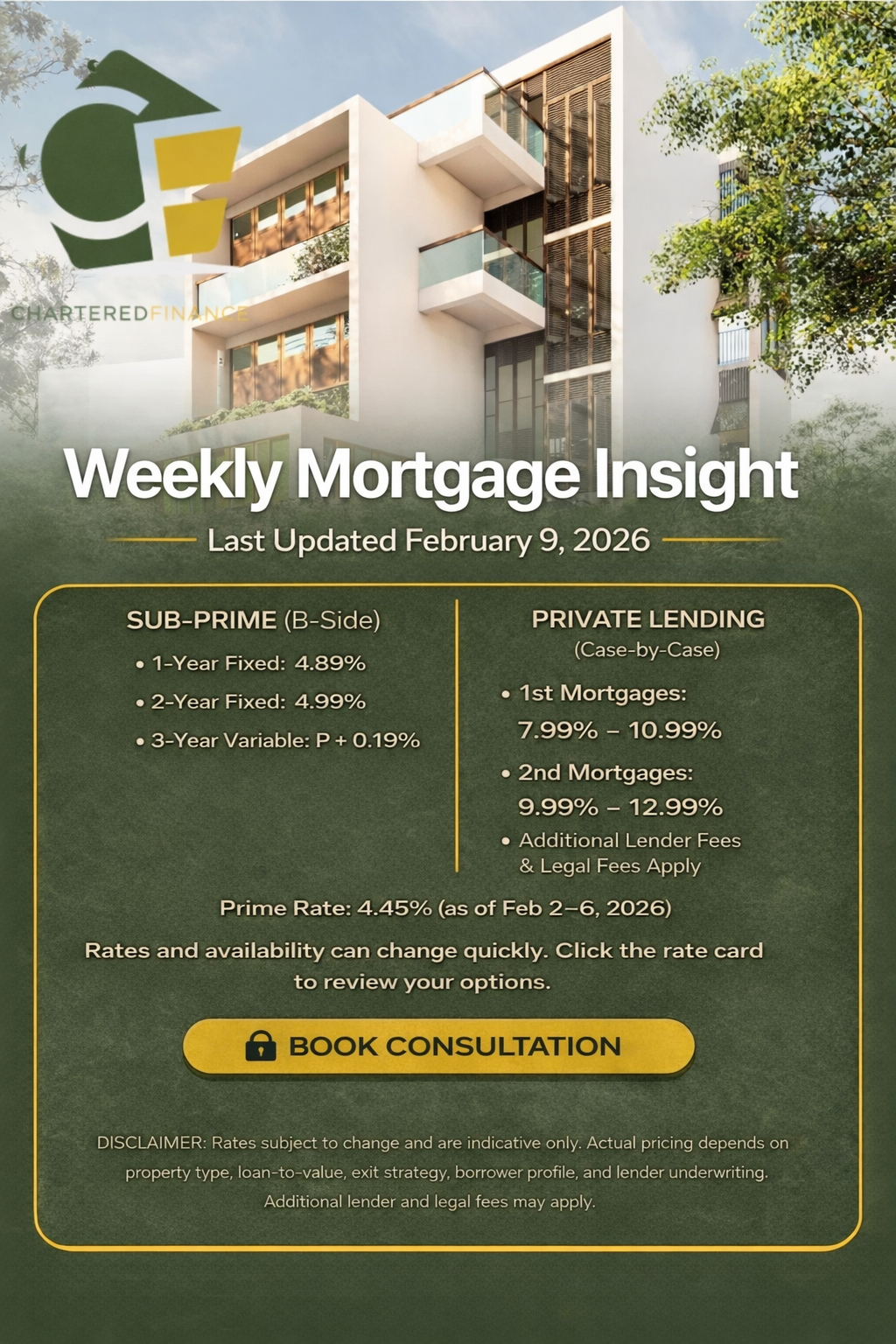

February 2–6, 2026

• B-side lenders remain active, but underwriting remains conservative this week.

• Variable-rate options continue to be priced cautiously.

• Private capital is strong for well-structured bridge and exit-driven files.

• Power of sale and arrears situations continue to attract competitive private funding.

• Clear exit strategies and verified equity remain the key drivers of approval and pricing.

👉 Rates and availability can change quickly. Click the rate card to review your options.

30-second overview

.png)

Free Guide: Smart Mortgage Solutions — When the Bank Says No

Alternative mortgages aren’t one single product. Depending on your equity, timeline, and income situation, there are several different lending routes that may make sense — each with its own pros, costs, and best-use scenarios.

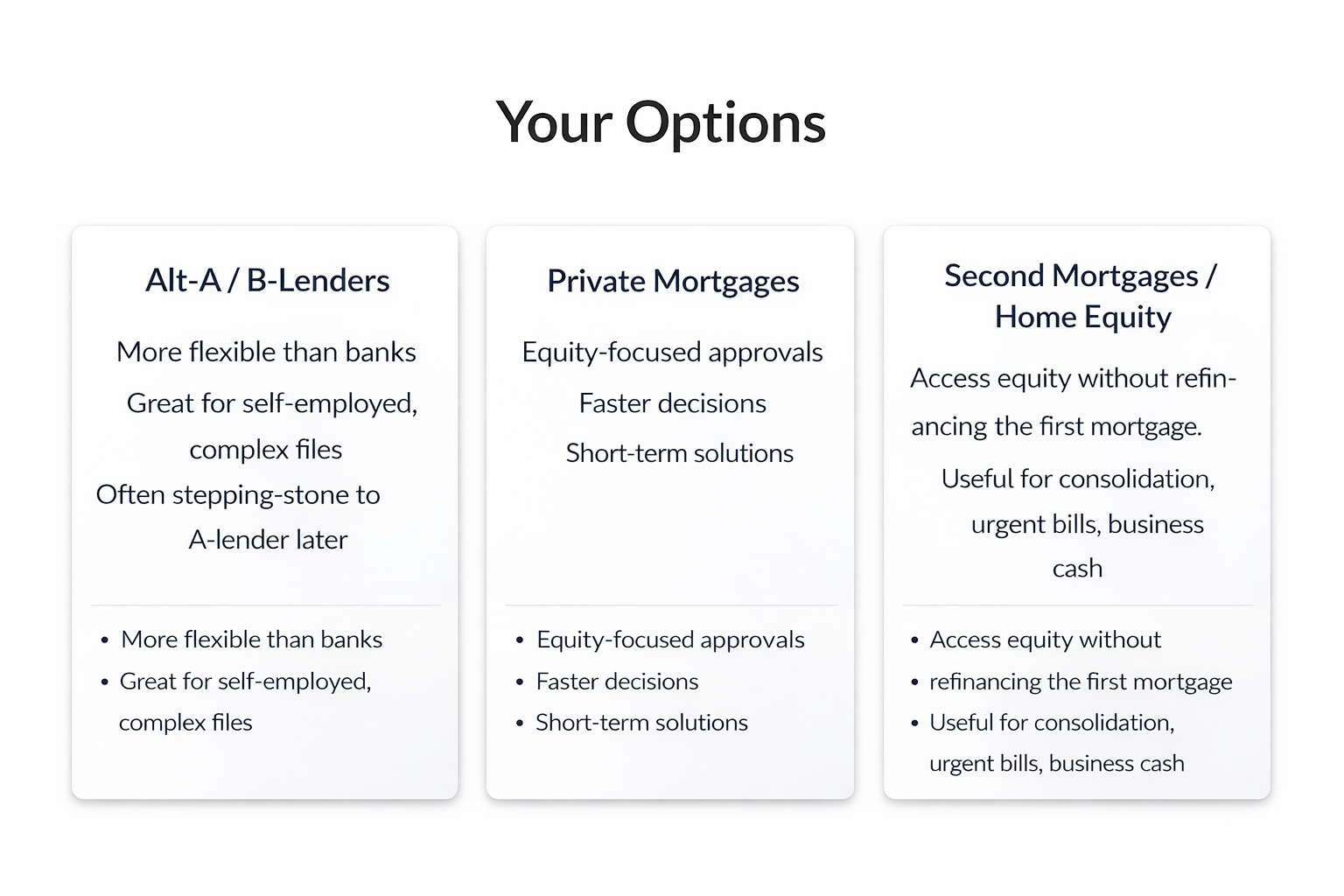

A strong middle ground between banks and private lenders. B-lenders may approve files that don’t meet strict bank rules, especially for self-employed income, credit history issues, or non-standard documentation.

• Often 1–3 year terms

• More flexible qualification

• Higher rates than banks, lower than private

A second mortgage is added behind your existing first mortgage, letting you access equity without breaking or refinancing your current mortgage.

• Useful for debt consolidation, renovations, or urgent cash needs

• Typically shorter terms

• Payments can be interest-only in some cases

Private lending is designed for flexibility and speed, and is often based primarily on equity. It can be a solution when banks and B-lenders can’t approve the file.

• Fast approvals and funding

• Equity-driven underwriting

• Higher rates and fees (trade-off for flexibility)

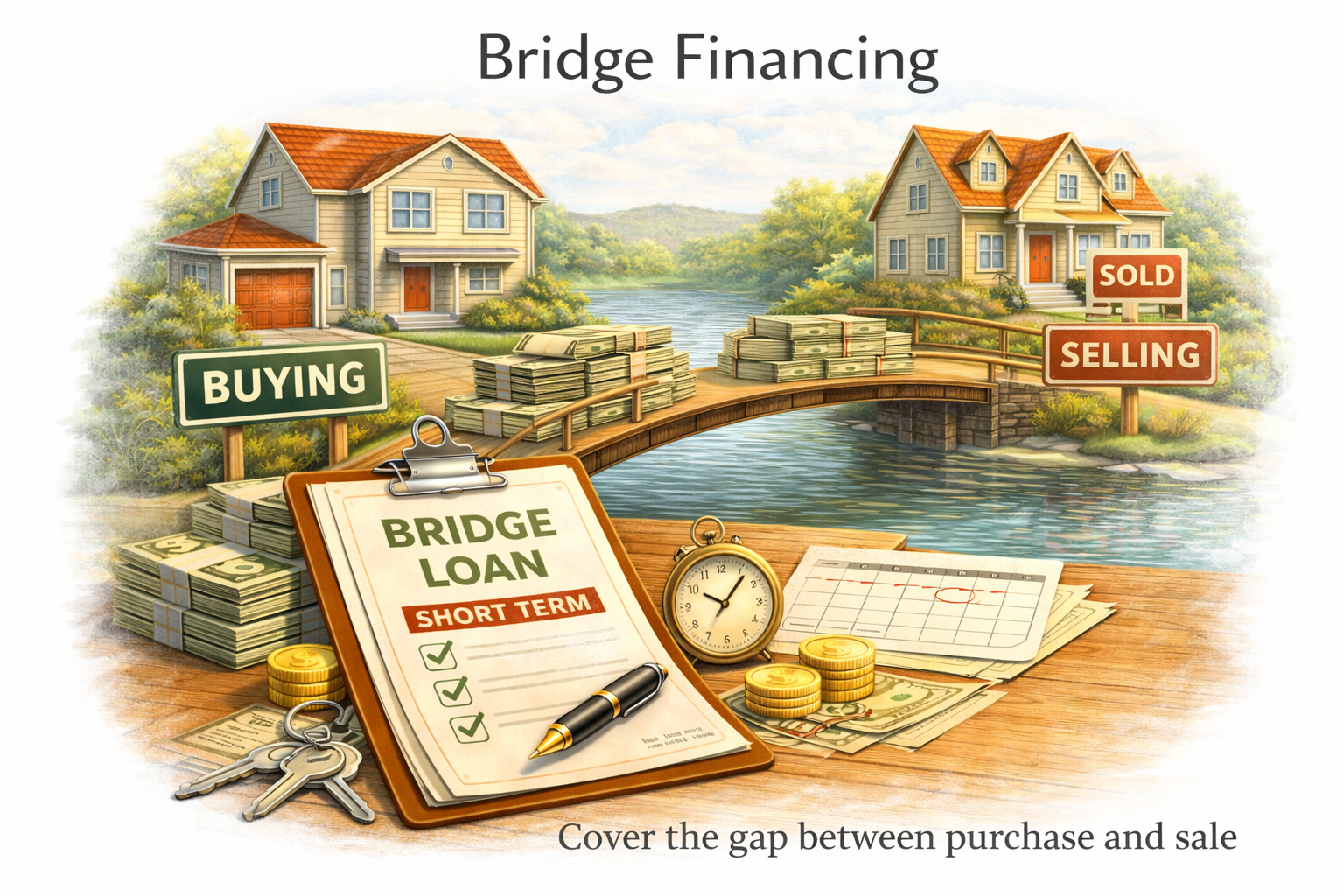

Bridge loans provide short-term financing to cover the gap between buying and selling a property. This is most common when timing doesn’t line up.

• Short duration (days to months)

• Helps avoid rushed decisions

• Requires clear exit timing

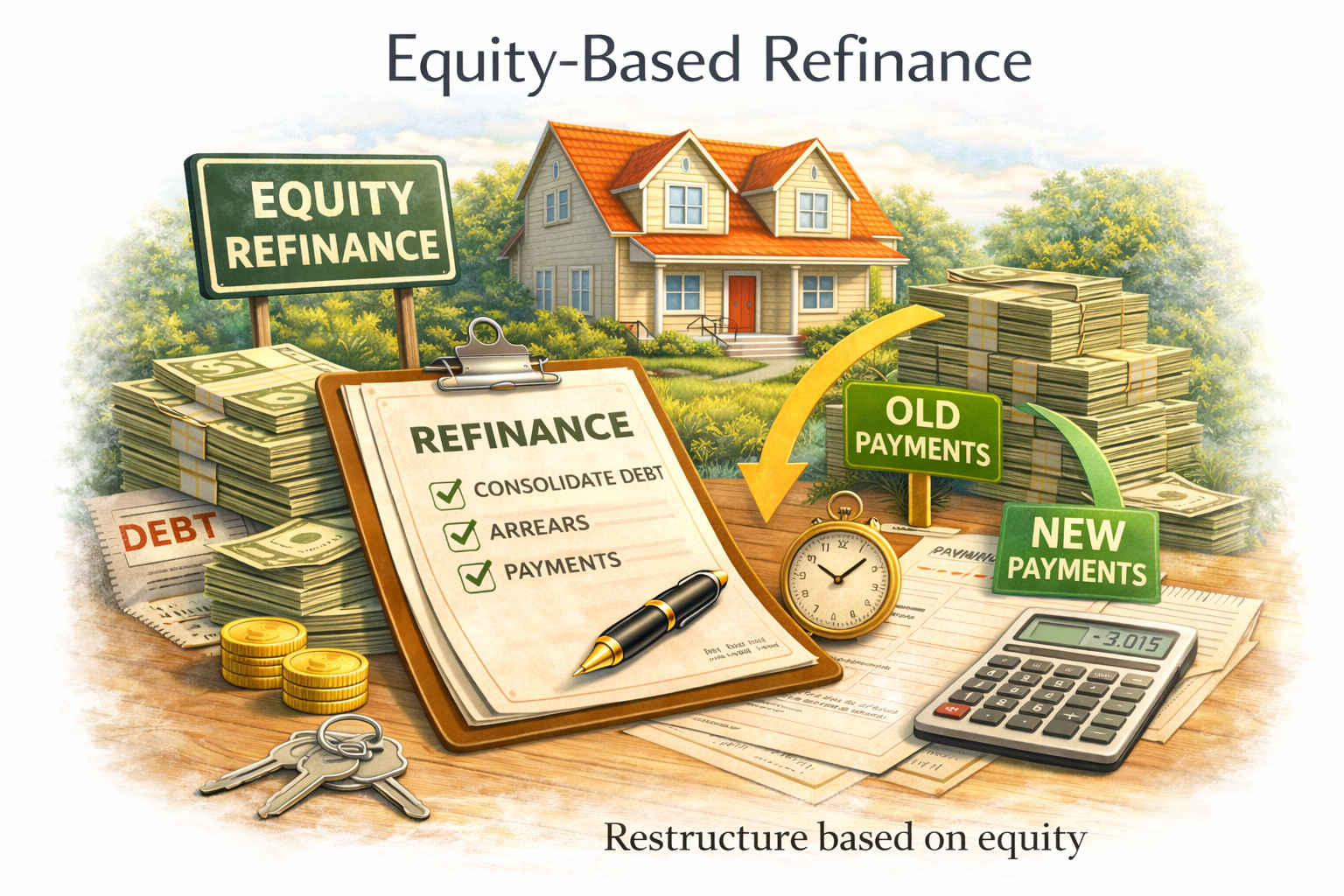

This approach restructures your mortgage based on equity and affordability — often used to consolidate debt, pay off arrears, or improve cash flow.

• Can lower monthly obligations

• May include a second mortgage or full refinance

• Requires a realistic plan for the next step

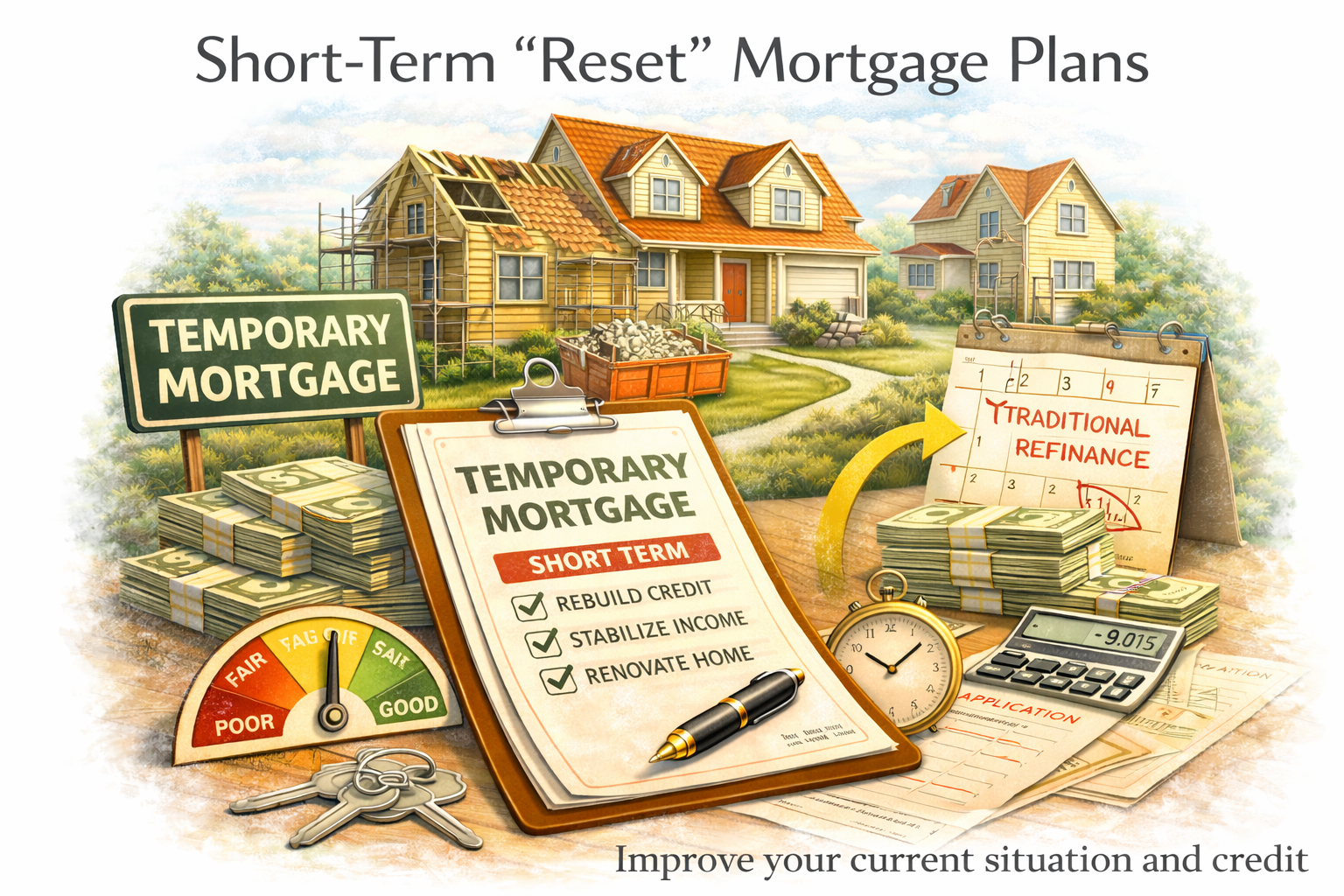

Some homeowners use alternative lending as a temporary solution while they rebuild credit, stabilize income, or complete renovations — then refinance back into a traditional mortgage later.

• Not meant to be permanent

• Works best with a clear exit plan

The best option depends on your timeline, your equity position, and what the next 12–24 months realistically looks like

• Higher Approval Rates ( Low Credit Or Irregular Income)

• Flexible Income Options (Self-Employed, Commission, Rental)

• Can Consolidate High-Interest Debt Into One Lower Payment

• Access Equity Without Selling Your Home

• Shorter Terms = A Faster Path Back To A-Lender Financing

• Solutions For Unique Properties (Rural, Unique Construction, Non-Conforming)

• Higher Interest Rates Than Traditional Banks

• Lender Fees & Broker Fees May Apply

• Stricter Exit Strategy Requirements (Refinance, Sale, Or Improvement Plan)

• Shorter Renewal Cycles (Often 1–3 Year Terms)

• Some Products Have Prepayment Penalties If You Break Early

Alternative mortgages are designed to solve a problem now, while giving you a clear plan to transition into better rates later. The key is making sure the mortgage is structured with a realistic exit strategy from day one.

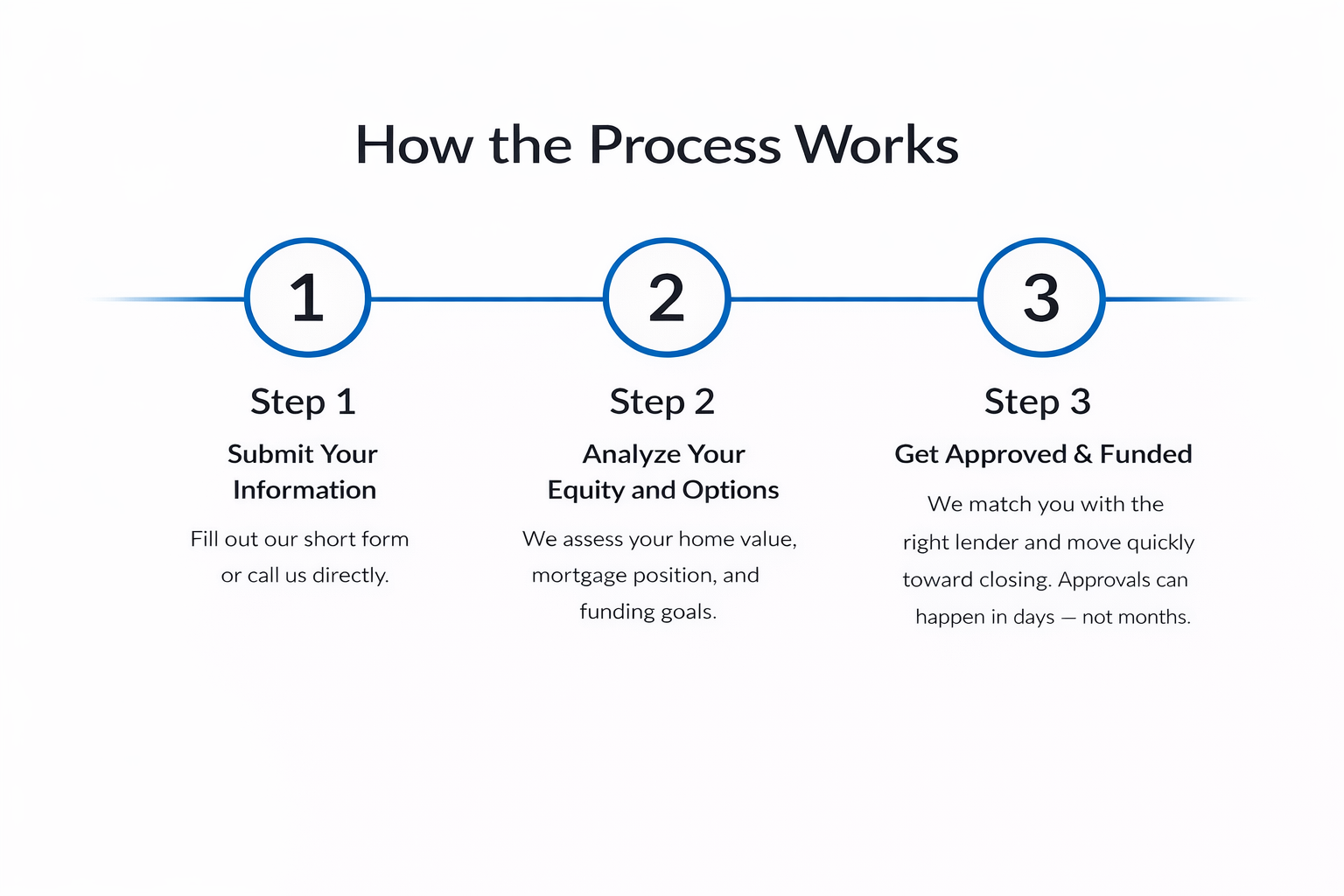

• A Straight Answer Up Front

We’ll tell you quickly what’s possible, what’s not, and what makes the biggest difference in approval

• A Plan Built Around Your Full Situation

Credit, income, equity, property type, and timeline — we structure the mortgage around the full picture, not one number

• Multiple Lenders Compared For The Best Fit

We review options across alternative lenders, including B-lenders and private lenders when needed

• Clear Terms, Fees, And Exit Strategy

No surprises. You’ll understand the rate, fees, term length, and the plan to move forward (refinance, renew, or sell)

• Fast Turnaround When Time Matters

If you’re facing a deadline, renewal pressure, or a power of sale situation, we prioritize speed and execution

• Support From Application To Funding

We handle the lender communication, conditions, and paperwork so you’re not stuck chasing answers.

Alternative mortgages cost more than bank financing — but they can solve problems that traditional lenders won’t

Alternative mortgage rates vary based on risk, equity, and the lender type

• B-Lender Mortgages: Typically lower than private, higher than banks

• Private Mortgages: Typically higher, but faster + more flexible

• Second Mortgages: Often priced higher due to lien position

• Short-Term / Bridge Financing: Usually higher due to short timelines

These are normal in alternative lending and depend on the lender + complexity

• Lender Fee (Commitment / Setup Fee)

• Broker Fee (If Applicable)• Appraisal Fee

• Legal Fees (Borrower + Lender Legal)

• Lender’s Lawyer / Admin Fees

• Discharge / Payout Fees (If Replacing a Mortgage)

Alternative lenders price based on speed, flexibility, and risk — not just credit score

• More flexible income verification

• Higher approval odds when banks say no

• Faster funding timelines

• Designed for short-term “reset” strategies

We focus on keeping the plan clear, affordable, and temporary

• We explain the real total cost before you commit

• We compare options across multiple lenders

• We build a next-step exit plan (refinance, sale, or restructure)

We help homeowners across Ontario get fast, confidential approvals — even with bruised credit or urgent timelines. No credit check required to start.

✔ Fast approvals

✔ Private lenders across Ontario

✔ No credit score minimum

✔ 100+ homeowners funded

✔ Fully confidential process

Rick Bettencourt, Mortgage Broker Level 2,

FSRA License #M11002425

licensed with Chartered Finance, Brokerage #12791

#302 – 7300 Warden Ave, Markham, Ontario.

Helping Ontario homeowners access practical mortgage solutions with clarity and confidence.

© 2025 Pure Mortgage Advisory Services. All rights reserved.